OLED New Cycle: Tandem Tech & Material Localization | CanChem

The global display market is witnessing a structural shift. According to recent market data, global smartphone shipments grew 8.5% YoY in late 2023, signaling a strong recovery in consumer electronics. More importantly, the OLED penetration rate continues to climb, surpassing50% and fundamentally challenging LCD dominance across all sizes.

1. The “Tandem” Effect: Why This Cycle is Different

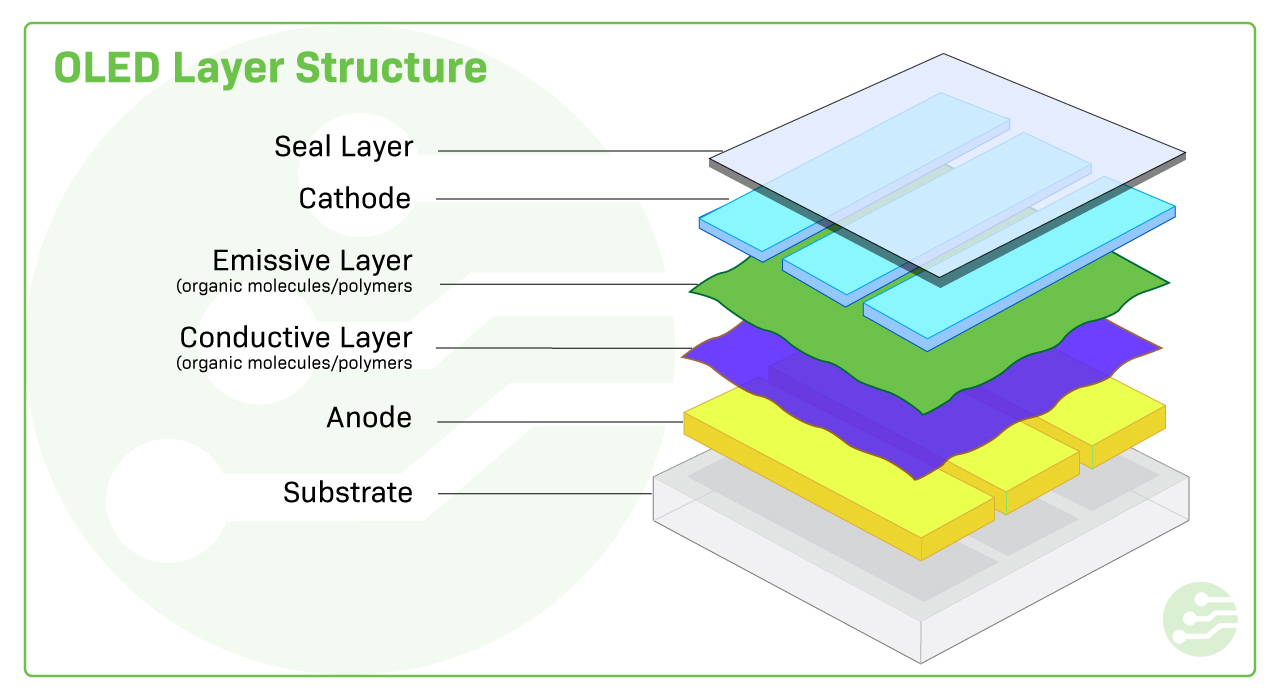

Unlike previous cycles driven solely by unit volume, this upturn is powered by a technology multiplier: Tandem OLED structures. First adopted by Apple’s iPad Pro (M4) in May 2024, Tandem stacks utilize two light-emitting layers instead of one, doubling brightness and quadrupling lifespan.

Market Impact For material suppliers, this is a game-changer. A Tandem structure effectively doubles the consumption of organic materials per panel area. As OLED expands from smartphones to tablets and laptops (IT panels), the total addressable market (TAM) for materials is projected to explode.

Market Impact

2. Expansion into IT Panels: The Next Frontier

While OLED dominates smartphones, its penetration in IT devices (Tablets, Laptops, Monitors) was only 1.4% to 1.9% in 2023. This represents massive headroom for growth.

Major panel makers like Samsung Display and BOE are aggressively investing in Gen 8.6 production lines, specifically optimized for mid-to-large size IT panels. Omdia forecasts that demand for OLED materials in IT applications will grow at a CAGR of 45% through 2028.

Smartphone Market

Stabilized growth with penetration >50%. The focus shifts to LTPO and folding screens to drive premium material mix.

IT Panel Market

Explosive growth phase (0 to 1). The iPad Pro launch is the catalyst, with MacBooks expected to follow by 2026.

3. The Rise of Domestic Materials

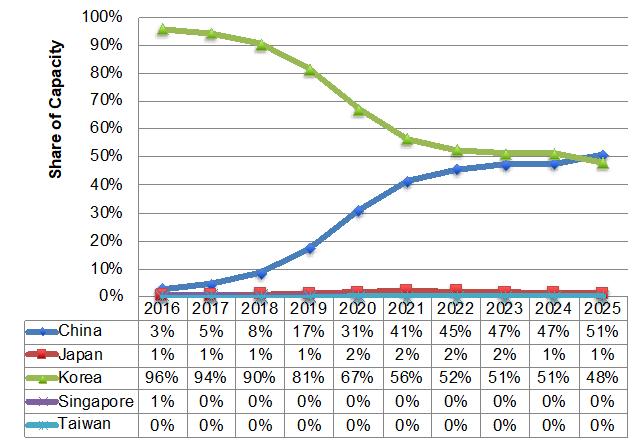

China’s OLED panel capacity now accounts for nearly 50% of the global total, breaking the Korean monopoly. However, the upstream material supply chain is still catching up. Domestic substitution is accelerating, particularly in terminal materials like Red/Green/Blue Prime layers and PDL (Pixel Definition Layers).

Leading Chinese players like Ruilian New Materials and Wanrun are moving from intermediates to high-value sublimation-grade materials, entering the supply chains of BOE and other giants.

Canchem Perspective

The OLED industry is entering a “super-cycle” driven by the dual engines of technological upgrade (Tandem) and application expansion (IT panels). For supply chain partners, the key to winning lies in securing positions within the new Gen 8.6 ecosystems and mastering sublimation-grade purity capabilities.

Canchem continues to monitor these critical upstream shifts, offering high-purity precursors and electronic chemical solutions to support the next generation of display technology.

Interested in Learning More?

Contact our team for technical specifications, sampling, or partnership inquiries.